There is a moment in every struggling business where time quietly changes sides.

In the early days of financial stress, time is still an ally. It gives directors room to think, to seek advice, to explore options. But left too long, time becomes unforgiving. Doors close. Choices narrow. What once might have been a restructuring conversation becomes a liquidation event.

Voluntary administration (VA) sits squarely in that shrinking window. It is not a last resort—but it does have a use-by date. This latest article from Bryan Williams explores when it it too late for voluntary administration, and why early action keeps options open for directors.

Voluntary administration is about timing, not rescue

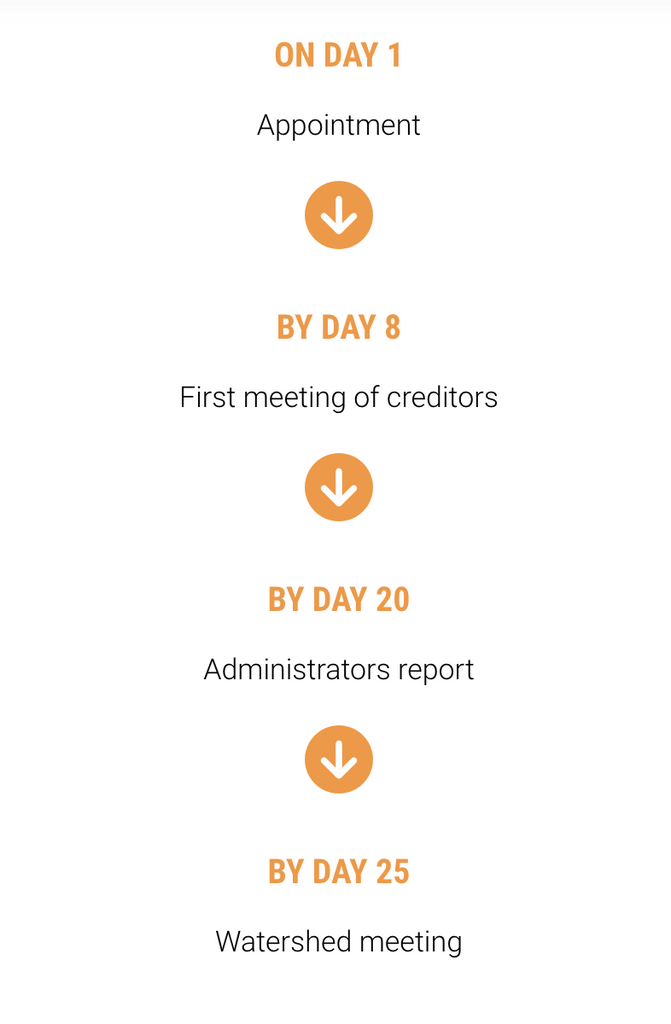

Voluntary administration was introduced into New Zealand law to give viable businesses breathing space when insolvency has only just begun to creep into the company’s state of affairs and has not yet consumed the business to the extent that liquidation is required.

At its core, the voluntary administration process is designed to achieve one of three outcomes:

- a return of the company to solvency,

- a better return to creditors than immediate liquidation, or

- an orderly exit that preserves as much value as possible.

What VA cannot do is reverse the consequences of inaction.

If assets have already been exhausted, creditor trust irreparably damaged, or funding options extinguished, voluntary administration may still occur, but its effectiveness will be limited to that of a salvage operation before a liquidator steps in. The process becomes more about managing decline than enabling recovery.

The narrowing window directors often miss

One of the recurring patterns we see at BWA Insolvency is not that directors fail to act but that they act too late.

By the time many businesses seek voluntary administration advice:

- cashflow has collapsed,

- key staff have departed,

- suppliers are trading on cash-only terms (or not at all),

- and secured creditors have issued statutory demands and are preparing their own enforcement action.

Once secured creditors appoint receivers, or enforcement action is already well advanced, the scope for voluntary administration to deliver a meaningful outcome reduces significantly.

VA is most effective when directors still have:

- operational control worth preserving,

- credible information to put before creditors,

- cash flow to support the continuation of the business while it undertakes restructure,

- and at least some commercial goodwill remaining.

When those elements are gone, the window has largely closed.

Insolvency is not a single moment

Many directors ask: “When does insolvency actually start?”

Insolvency is a process, not an event. It develops quietly—often months or years before it becomes visible on a balance sheet.

Insolvency occurs when a company is both cash flow and balance sheet insolvent. A company can tip between the two for years, be insolvent on paper, yet still have the funds to support the day-to-day operations of the business. It is during this period that Voluntary Administration is most critical and when business recovery is most likely.

Insolvency practitioners and the courts do not look for a dramatic collapse. They look at decisions made over time, based on the information available at the time. This matters because directors’ duties evolve as financial distress deepens. Once a company is insolvent, the directors’ duties expand to be owed not just to the company but also to the creditors it exposes by continuing to trade. When this occurs, there is the very real risk that a director may be exposed to claims based in breaches of duty.

At this point, the obligation to consider creditors’ interests becomes paramount.

The earlier advice is sought, the easier it is to demonstrate that those duties were taken seriously.

Why waiting feels logical (but isn’t)

From the outside, early voluntary administration can look premature. From the inside, delay often feels rational.

Directors hope the next contract will land. That the seasonal dip will pass. That one more refinance, one more capital injection, one more good month will restore equilibrium.

Sometimes it does. More often, it doesn’t.

As I often say, insolvency is always late to the party. By the time it shows up, the conditions that caused it have already been in play for some time.

When voluntary administration may already be too late

While every case is fact-specific, there are common indicators that the voluntary administration window is closing or closed:

- The business has no capacity to trade forward, even under protection

- There is no realistic funding pathway to support a restructure

- Secured creditors have lost patience and are moving independently

- Records are incomplete or unreliable

- The company’s value exists only in historic goodwill

A final thought for directors

The question is not “Is it too late?” The better question is: “What will still be possible if we act now?”

Voluntary administration is not about saving every business. It is about preserving value, credibility, and choice. And like most things in business, those who move early tend to keep more of all three.