BWA Insolvency

Quarterly Market Report: Q1 2026

Has business stress peaked? What the latest insolvency data tells us

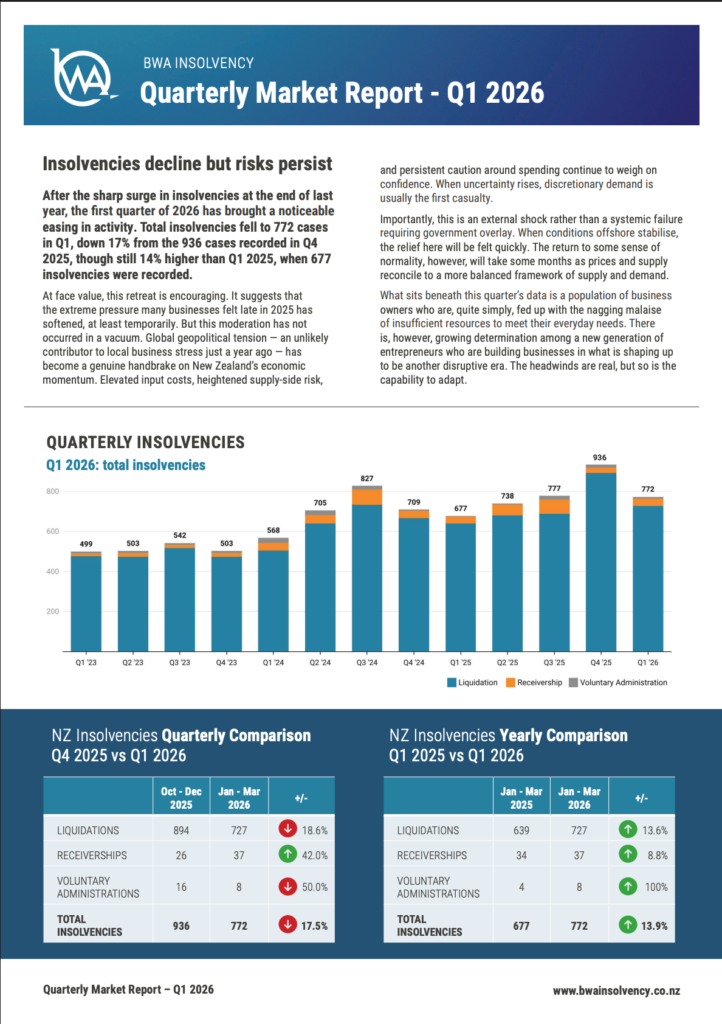

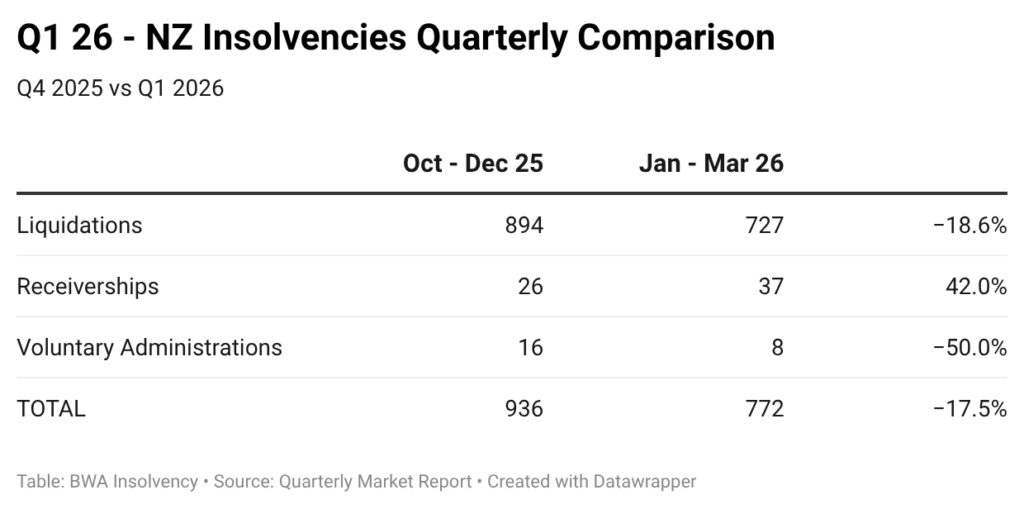

New Zealand insolvency activity eased in the first quarter of 2026, after a peak late last year. While the headline numbers suggest some relief, the underlying picture remains complex. For many businesses, the pressure is far from over.

BWA Insolvency’s latest Quarterly Market Report recorded 772 insolvencies in Q1 2026, down 17% from 933 in Q4 2025. Despite this decline, insolvencies remain 13.9% higher than the same quarter last year, indicating that financial stress continues to run deep across the business community.

A turning point, but not a recovery

The quarterly drop is encouraging, but it does not signal a full recovery. As BWA Insolvency principal Bryan Williams explains, current conditions are heavily influenced by global factors rather than purely domestic ones.

“The easing in quarterly results should not be mistaken for a full recovery, as the current geopolitical situation continues to affect the market. This is an external shock, not a home-grown economic failure. When offshore conditions stabilise, the relief here will be felt quickly — although a full return to normality will take time as prices and supply rebalance.”

Elevated input costs, ongoing supply chain risks and cautious consumer spending continue to weigh on demand, leaving many businesses exposed.

By type, liquidations continue to make up the vast majority of insolvency activity.

- 727 liquidations were recorded in Q1 (down 18.6% on Q4, but still up 13.6% year-on-year)

- 37 receiverships, up 42% on the previous quarter

- 8 voluntary administrations, indicating fewer distressed businesses are pursuing formal restructuring pathways

The relatively low level of voluntary administrations suggests many businesses are still at a point where recovery options are limited.

Insolvency activity remains heavily concentrated in New Zealand’s main centres:

- Auckland: 465 cases (around 60% of the national total)

- Canterbury: 132 cases

- Wellington: 63 cases

Industry Spotlight

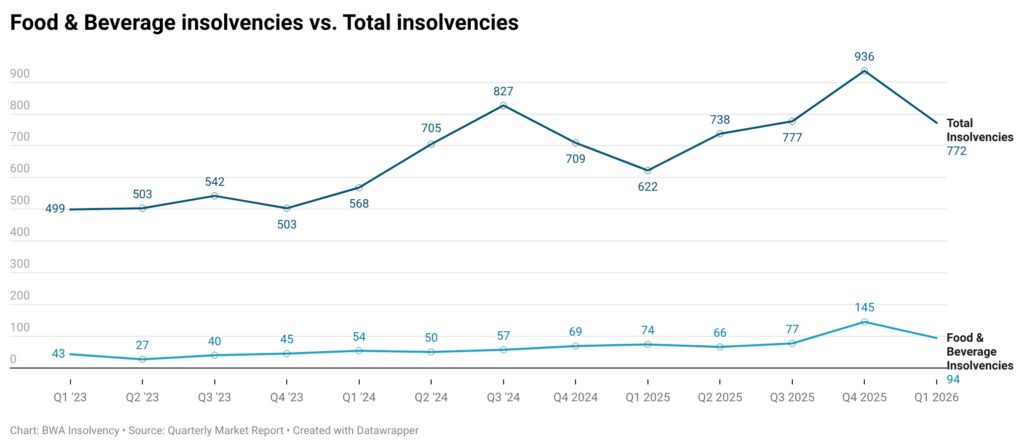

Several consumer-facing sectors recorded notable quarter-on-quarter declines, suggesting short-term stabilisation.

- Food and beverage: down 36% compared to Q4, but still 31% higher year-on-year

- Retail trade: down 57%

- Property and real estate: down 29%

Despite this, recent high-profile hospitality liquidations highlight ongoing strain in the sector, particularly for operators dependent on discretionary spending.

Construction remains the standout area of concern, recording the highest number of insolvencies by volume, with 215 cases in Q1, slightly up on the previous quarter. This underscores the ongoing structural challenges facing the industry.

Looking ahead, conditions are likely to remain difficult, particularly for businesses reliant on discretionary consumer spending.

“Consumer-facing sectors will find the next few months difficult. The onset of winter will amplify the consequences that flow from troubled countries. The hardest hit will be those that rely on discretionary spending, with demand likely to drop significantly,” says Williams.

Seasonality, combined with continued global uncertainty, is expected to put further pressure on already fragile balance sheets.

While trading conditions may improve gradually, many businesses are still carrying the financial legacy of the COVID and post-COVID period.

“There are still many companies with lean balance sheets as a result of COVID and the post-COVID era. Many have accumulated obligations to Inland Revenue, and it is only a matter of time before those are addressed — or liquidation will result.”

This underlying stress means insolvency activity could remain elevated even as broader economic conditions begin to stabilise. Despite current challenges, there are signs of resilience across the New Zealand business community.

“Behind this current disturbance lie New Zealanders who have had enough of the nagging malaise associated with having insufficient resources to meet everyday needs. There is evidence of spirited potential among a wave of innovative, tech-driven and AI-focused businesses shaping the future economy.”

New Zealand’s fundamentals remain strong, and the economy is well-positioned to respond when global conditions improve.

Looking ahead

Q1 data suggests we may have passed the peak of business distress, but the recovery path is unlikely to be smooth or immediate.

For business owners, lenders and advisors, the coming months will require careful navigation, particularly in sectors exposed to consumer demand and cost volatility.

The full Quarterly Market Report provides a deeper analysis of sector trends and regional activity, offering a detailed view of where pressures remain — and where opportunities may emerge.

The full Quarterly Market Report is available here.